Omnis Weekly Update May 15th

Posted by Nigel on Monday 15th of May 2023

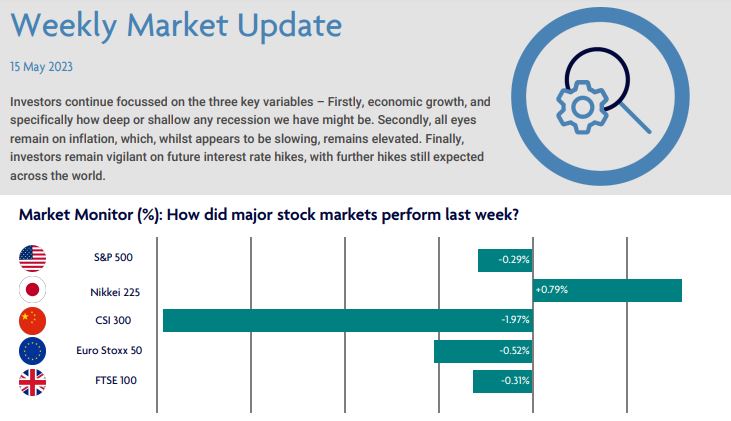

US: Investors weigh inflation data and concerns on debt ceiling

Headline consumer price inflation slowed to 4.9% over the year ending in April, the slowest pace in two years. Despite this, there are still policymakers suggesting that it would be unlikely that interest rates would come down this year. Along with banking stresses and tightening credit conditions, another factor weighing on sentiment seemed, to the upcoming deadline, to increase the debt ceiling. U.S. Treasury Secretary Janet Yellen has warned that the deadline could come as e...

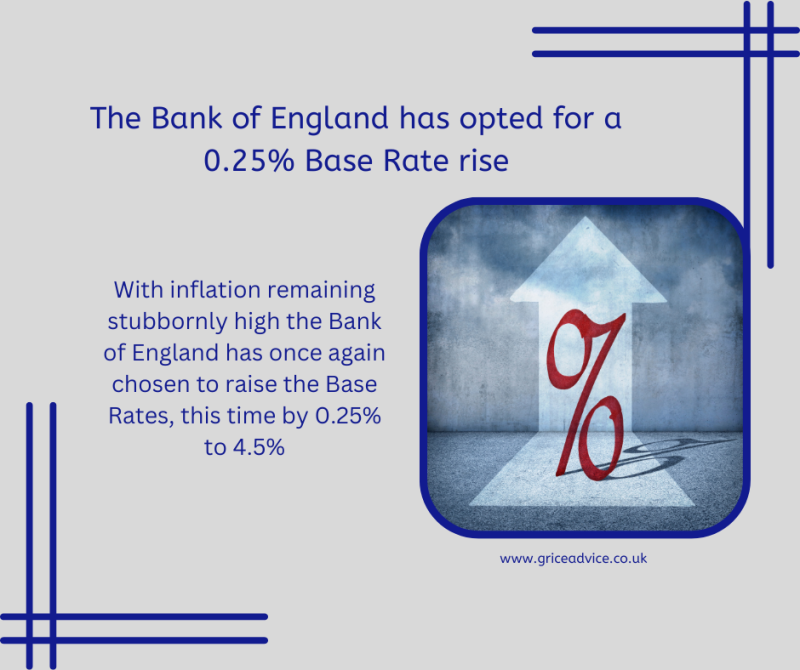

Bank of England base rate rise - May 23

Posted by Nigel on Thursday 11th of May 2023

The rise in the BoE rate to 4.5% was predicted in the markets and comes on the back of the Fed (US) and ECB (European) rate rises last week. The long-term forecast is for inflation to fall this year, but as inflation is proving harder to reduce the Bank has again, increased rates today.

What does this mean for you?

If you have a mortgage:

Fixed rate: your monthly payments won't be affected right now.

Tracker rate: you will already have seen an increase to your monthly payments and are likely to see further rises.

Variable rate: you may ...

Buying your first home

Posted by Nigel on Wednesday 10th of May 2023

Looking for your first home, but the mortgage market is huge and you’re not sure which lender is right for you or how to go about it. What next?

Our infograph below may help.

Omnis Weekly Update May 9th

Posted by Nigel on Tuesday 9th of May 2023

US: Higher interest rates for longer?

As expected, the Federal Reserve raised interest rates by 0.25% points but indicated that they did not expect to cut interest rates as quickly as investors might expect. The prospect of higher interest rates for longer weighed on markets, as did the increasing uneasiness surrounding the need to raise the US debt ceiling, with indications that the US might not be able to meet its debt obligation as early as June. Volatility in the shares of regional banks rose as further regional banks look for lifelines...

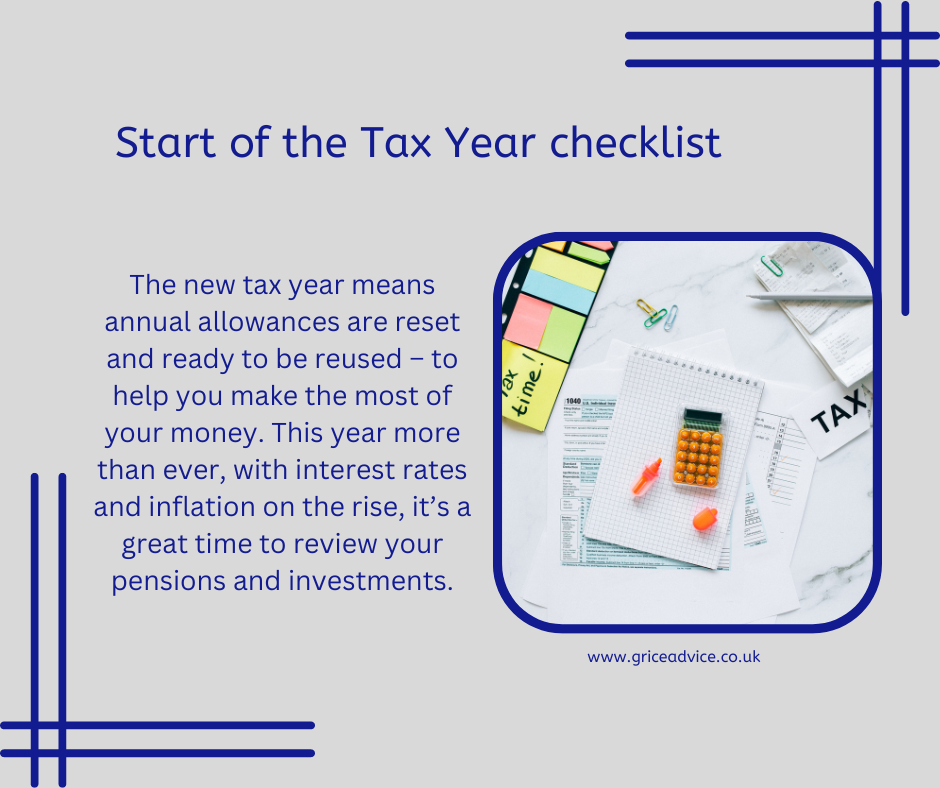

Tax Check List - organise yourself for the year ahead

Posted by Nigel on Wednesday 3rd of May 2023

The new tax year on 6 April 2023 is a great time to review your finances.

The new tax year means annual allowances are reset and ready to be reused – to help you make the most of your money. This year more than ever, with interest rates and inflation on the rise, it’s a great time to review your pensions and investments.

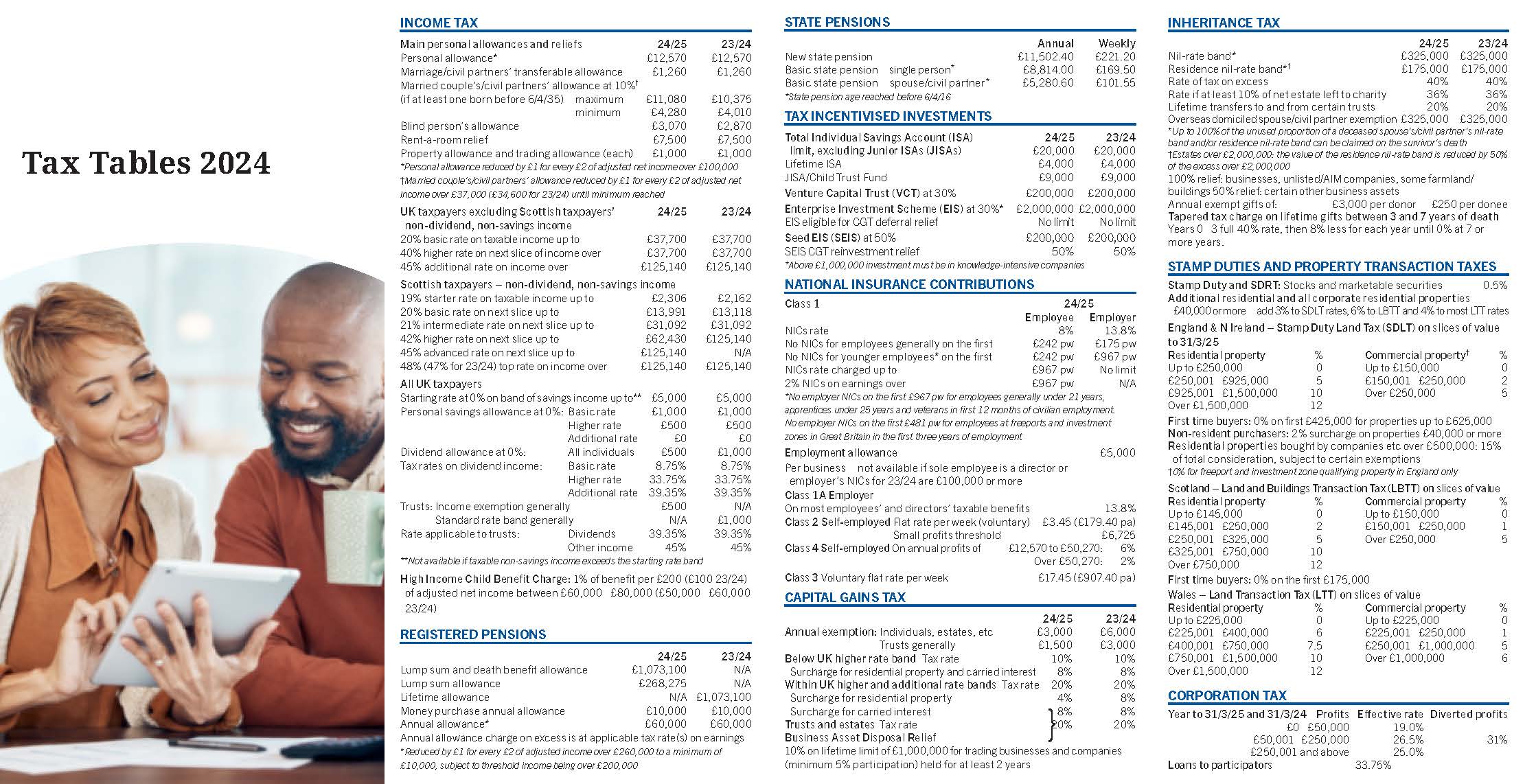

Note: The following figures apply to the 2023/2024 tax year, which starts on 6 April 2023 and ends on 5 April 2024.

ISAs

The maximum you can invest across your ISAs is £20,000 (if it’s a cash ISA, stocks and shares ISA o...

The Chancellor of the Exchequer Rachel Reeves outlined planned reforms to the welfare system, boosts to investments in economic growth and heightened focus on closing the tax gap.

Amidst growing uncertainty over the conflict in Ukraine and the impacts for European security, alongside rising instability caused by Donald Trump’s tariff war, the Spring Statement 2025 built on the government’s announcements last autumn with a renewed commitment to financial stability.

In laying out the Spring Statement, Rachel Reeves said: ‘the global economy has become more uncertain, bringing insecurity at home as trading patterns become more unstable and borrowing costs rise for many major economies.’

She added that the UK was ‘one of the world's largest economies, an ally to trading partners across the globe and a hub for global innovation. These strengths and the progress that we have made so far mean that we can act quickly and decisively in a more uncertain world to secure Britain's future and to deliver prosperity for working people.’

Reeves' last announcement, made in October 2024, included boosts to minimum wages, an increase in the state pension and a reduction to the headline rate for National Insurance. Now, however, the government has opted for an alternative strategy with major initiatives aimed at courting homeowners and small business owners, among others.

So, ultimately, who wins and loses? Let's explore which groups could be most affected by these changes.

WINNERS

Builders and Property Developers.

The Chancellor made a firm commitment to solving the housing crisis. Changes to the National Planning Policy Framework alone are slated to help build over 1.3m homes in the UK over the next five years.

Education Secretary Bridget Phillipson also pledged more than £600m to train 60,000 construction workers and address widespread skills shortages in the construction sector. This measure and others could benefit home builders, architects, town planners and other associated professions through government aid and streamlined planning permission regulations.

Property Owners.

Reeves’ planning reforms aim to boost house building to a 40-year high and stimulate more activity in the housing market. The Office for Budget Responsibility (OBR) predicts these reforms could permanently increase real GDP by 0.2% in 2029/30, translating to an additional £6.8 billion for the economy.

That kind of economic stability could drive increases in property values and benefit homeowners looking to sell in the next five years.

The Defence Industry.

Defence spending will increase to 2.5% of GDP, putting an extra £6.4bn into the sector by 2027. This uptick will be funded by cuts to the overseas aid budget, bringing it down to 0.3% of GDP.

The Chancellor suggested this would save approximately £2.6bn in day-to-day spending in 2029/30 and help to fund more capital investments. Expect a boost to defence sector growth in the years to come.

Certain Tech Companies.

Technology companies in the defence sector stand to benefit significantly from Reeve’s plans. The Ministry of Defence will spend at least 10% of its equipment budget on cutting-edge technology thanks to a dedicated £400m innovation pot.

Elsewhere, Reeves pledged to up investments into artificial intelligence (AI) to modernise government services and increase efficiencies.

Unemployed Young People.

The Spring Statement also included a clear message that if young people can work, they should be given the opportunity to do so. The Chancellor unveiled a series of measures designed to help get young people into work, including the establishment of 10 new technical excellence colleges across every region of the country and new opportunities for skills development.

LOSERS

Benefits Claimants.

The government plans to reshape the benefits system and focus on getting people into work. The Universal Credit Standard Allowance for a single person aged 25 or over will see a modest increase from £92 to £106 a week by 2029/30.

Offsetting this, however, are planned cuts and freezes to other aspects of Universal Credit. The health element will be frozen for existing claimants until 2029/30. It’ll be reduced to £50 a week for new claimants in 2026/27 and then frozen until 2029/30.

These changes are part of a broader strategy to reduce welfare spending as a share of GDP. The government emphasises that the reforms will make the system more sustainable while pushing more people into employment. However, for many current and potential benefit recipients, this means navigating a more challenging landscape with potentially reduced financial support.

Healthcare Workers.

Reeves reiterated her commitment to dismantle NHS England, stating: ‘the Prime Minister set out plans to abolish the arms-length body NHS England and ensure that money goes directly to improving the service for patients [...] the Health Secretary is driving forward vital reforms to increase NHS productivity, bearing down on costly agency spending to save money so that we can improve patient care.’

Proponents say the decommissioning will remove inefficiencies and unnecessary bureaucracy, but others claim the measures could result in the loss of up to 30,000 jobs.

Civil Service Workers.

The Chancellor outlined significant reforms to reduce the size and cost of the civil service. The government will introduce voluntary exit schemes to allow employees to leave their positions voluntarily, reducing overall staff numbers without mandatory redundancies.

Additionally, the government will invest in AI to increase efficiency and reduce civil service running costs by 15% (amounting to £2bn in savings) by the end of the decade. While Reeves framed these changes as part of a broader strategy to create a leaner state, they could represent a threat to job security for civil service workers.

What’s Next?

The 2025 Spring Statement included several key initiatives to level up Britain's defences, address the housing crisis and crack down on taxation fraud.

The Chancellor appeared confident that these measures combined with agile responses to global instability would drive growth and see the average British household £500 a year better off than this government compared to the last.

It’s clear that appetite for economic and policy reform is strong on the Labour frontbenches. These changes combined with the raft of measures announced last October are shifting the way many people approach their finances.

Feel free to get in touch if you have any concerns about the impact of these changes on your situation or if you want to explore the opportunities they might create.

The value of investments and any income from them can fall as well as rise and you may not get back the original amount invested.

HM Revenue and Customs practice and the law relating to taxation are complex and subject to individual circumstances and changes which cannot be foreseen.

Approved by The Openwork Partnership on 26/03/2025